What are Scope 1, 2, and 3 Greenhouse Gas Emissions?

By Celetia Sahadave, WKC Group

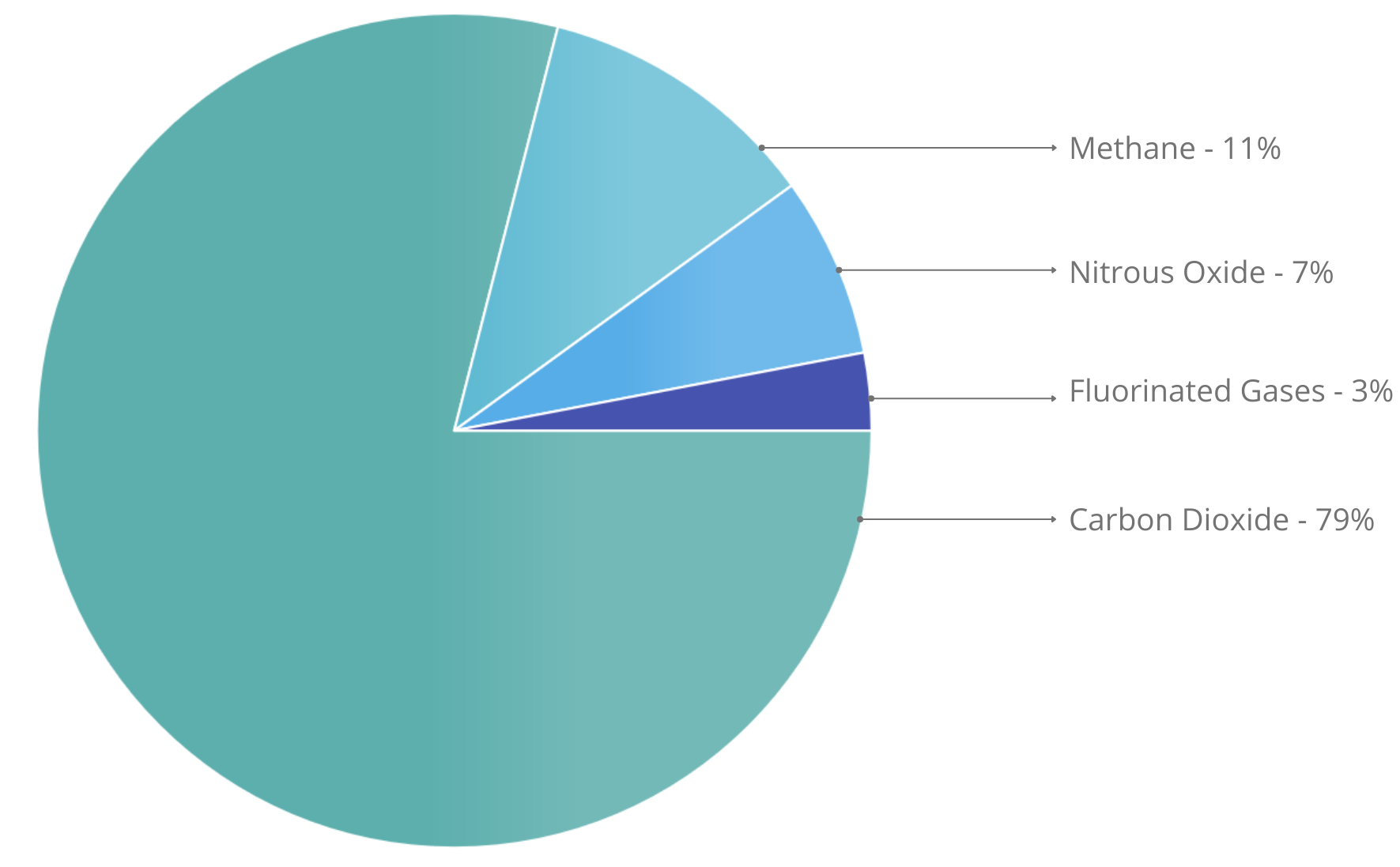

What are GHGs?

A greenhouse gas (GHG) is a gaseous compound with the ability to trap heat (or longwave radiation) in the Earth’s atmosphere. This results in high temperatures being retained in the lower atmosphere, thus allowing less heat to escape back to space. Common GHGs present in the atmosphere include fluorinated gases (chlorofluorocarbons (CFCs) (e.g., tetrafluoromethane (CF4)) and hydrofluorocarbons (HFCs)), carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), and ozone (O3).

Overview of Emissions by GHG Type

What is the Greenhouse Gas Protocol (GHGP)?

The GHGP establishes global standardised frameworks to measure and manage GHG emissions from private and public sector operations, value chains and mitigation actions. The GHGP has developed calculation tools for the three main categories associated with GHG reporting, namely:

- Scope 1;

- Scope 2; and,

- Scope 3.

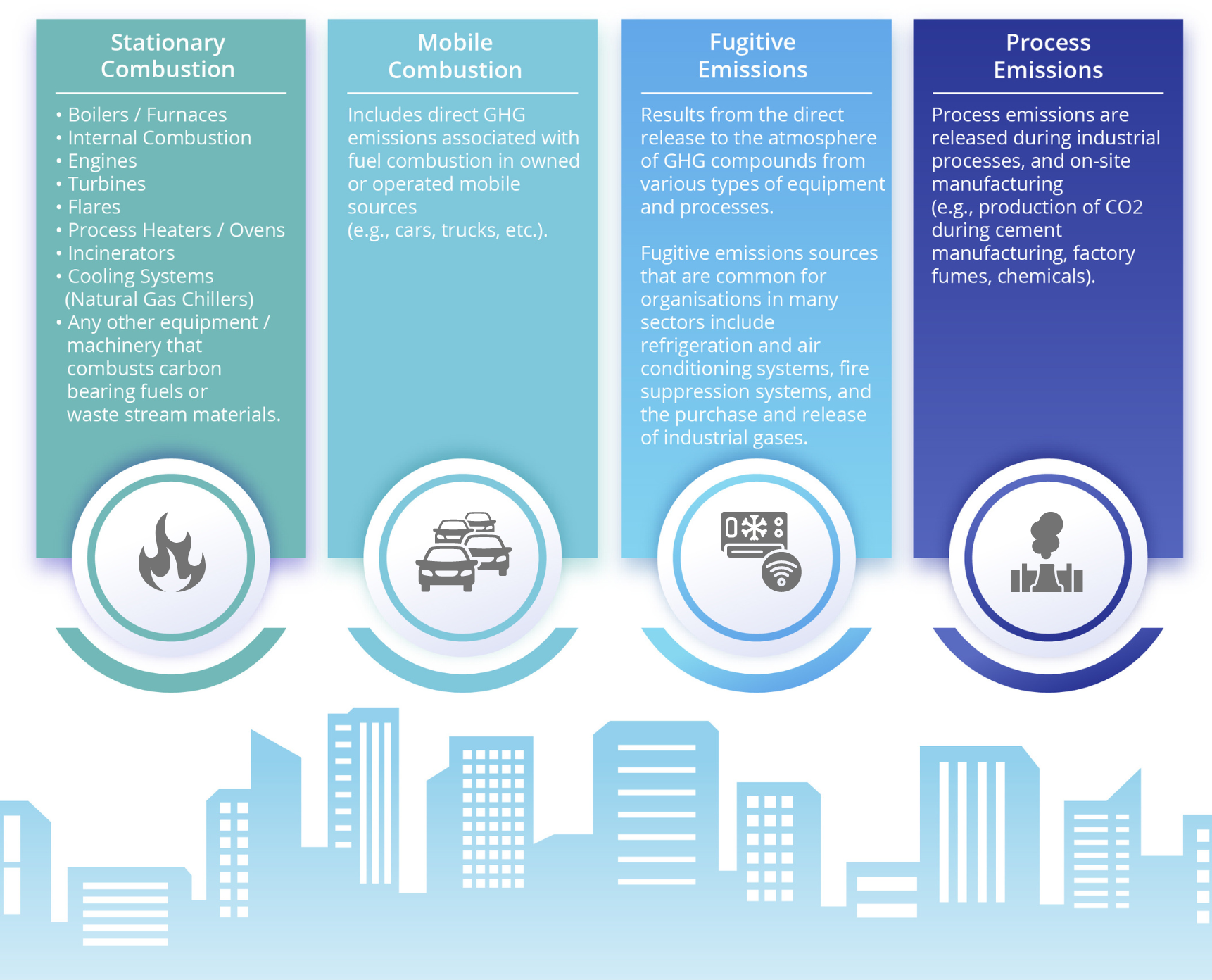

Scope 1 Emissions

Scope 1 emissions are direct GHG emissions from sources that an organisation owns or controls directly. These emissions can be divided into four categories such as stationary combustion, mobile combustion, fugitive emissions and process emissions. Examples of emissions from each category are provided below.

Scope 2 Emissions

Scope 2 emissions are indirect GHG emissions associated with the generation of purchased energy, and usually occur at the facility where they are generated. In other words, all GHG emissions released to the atmosphere, from the consumption of purchased electricity, steam, heat and/or cooling.

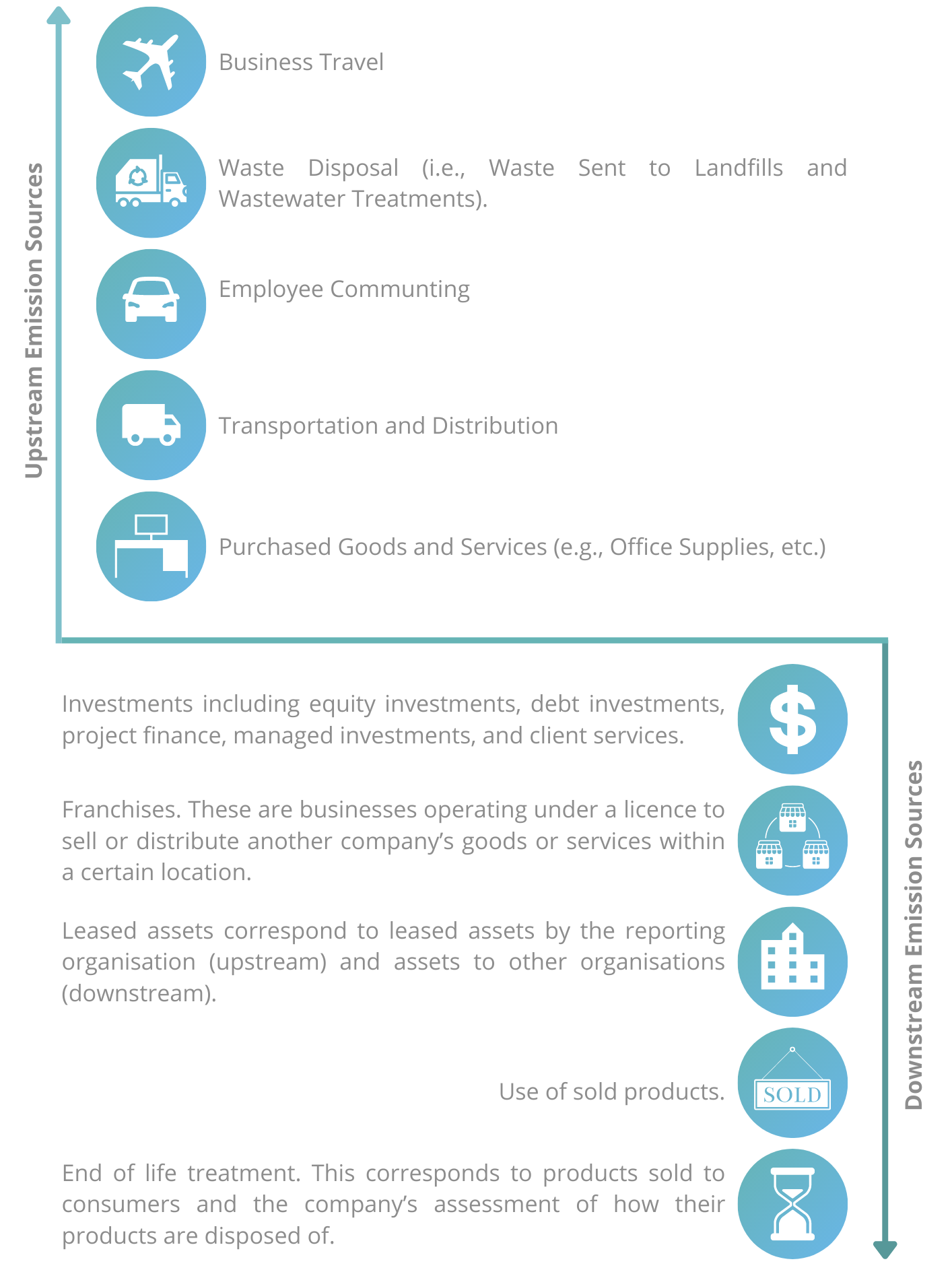

Scope 3 Emissions

Scope 3 emissions are the result of activities from assets not owned or controlled by the reporting organisation, but that the organisation indirectly impacts in its value chain. Scope 3 emissions include all sources not included within Scope 1 and Scope 2 emissions. Scope 3 emissions can be categorised as either upstream or downstream emissions.

Why Quantify GHG Emissions in a Project Finance Context?

For Projects seeking finance from an Equator Principle Financial Institution (EPFI), the Equator Principles requires clients to report GHG emissions where GHG emissions (combined Scope 1 and Scope 2 Emissions) exceed 100,000 tonnes of CO2 equivalent annually. Reporting is undertaken for the operational phase of the Project (i.e. following Project Completion) over the life of the loan (i.e. whilst repayments are being made). It is important to note that for all projects, when combined Scope 1 and Scope 2 GHG emissions are expected to be more than 100,000 tonnes of CO2 equivalent annually, a Climate Change Risk Assessment (CCRA) is required.

On a similar note the World Bank Group / International Finance Corporation Performance Standard 3 thresholds for reporting GHG have been reduced from 100,000 tonnes CO2 to 25,000 tonnes of CO2 per year. This means that any project being financed by the IFC (or any lenders that adopt the guidelines) will be required to report on the Project emissions where these are expected to exceed 25,000 tonnes per annum.

Contact WKC’s team of consultants for more information on GHG Emission Inventories and Climate Change Risk Assessments or read through our previously published article which highlights the important aspects of a Climate Change Risk Assessment.